Case Study: How Zomato Finally Became Profitable - The Real Math No One Shows You

Hello and welcome back to The Finance Lens!

For years, Zomato was the punchline of every startup joke: “loss-making,” “unsustainable,” “too much discounting,” “will never turn profitable.” Everyone used the app, but nobody believed in the business. And yet, quietly, without hype or noise, Zomato engineered one of the most impressive financial turnarounds in India’s tech history. This case study is not just about numbers; it is about how a company restructured itself, bet big on the right businesses, and proved an entire market wrong.

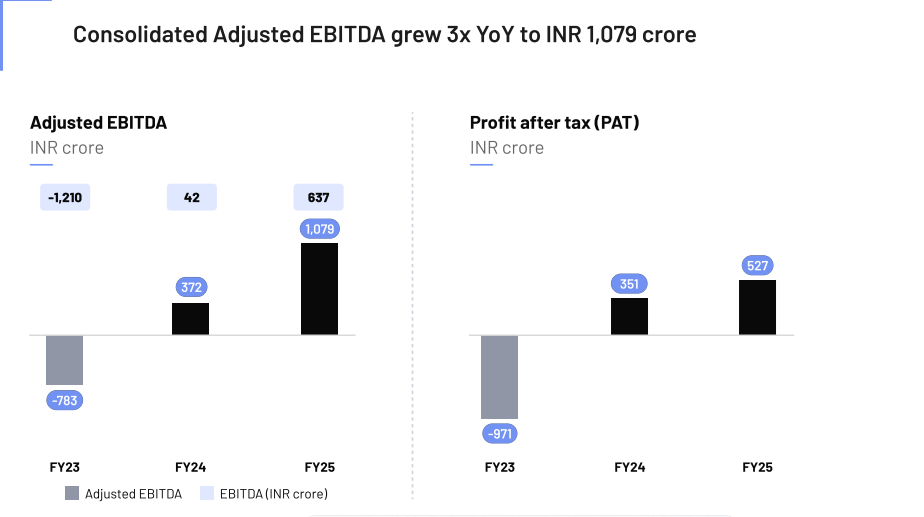

And then it happened, Zomato reported profitability. Not for a single lucky quarter, but consistently, while also growing faster than ever.

This deep dive explains exactly how they did it, using:

simple, clear math

FY22 → FY25 financial data

comparisons with Swiggy

insights from Blinkit, Hyperpure & Going-Out

key profitability inflexion points

risks

and valuation

Let’s lift the hood and break it down step by step.

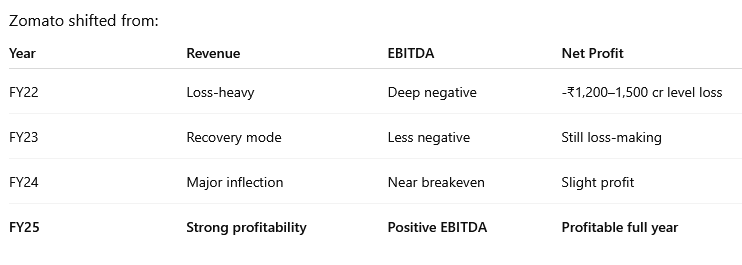

1. The 4-Year Journey: FY22 → FY23 → FY24 → FY25

This was not luck. It was four compounding levers:

1. Order volume explosion

2. AOV stability

3. Better delivery cost optimisation

4. Blinkit scale kicking in

Let’s decode each one.

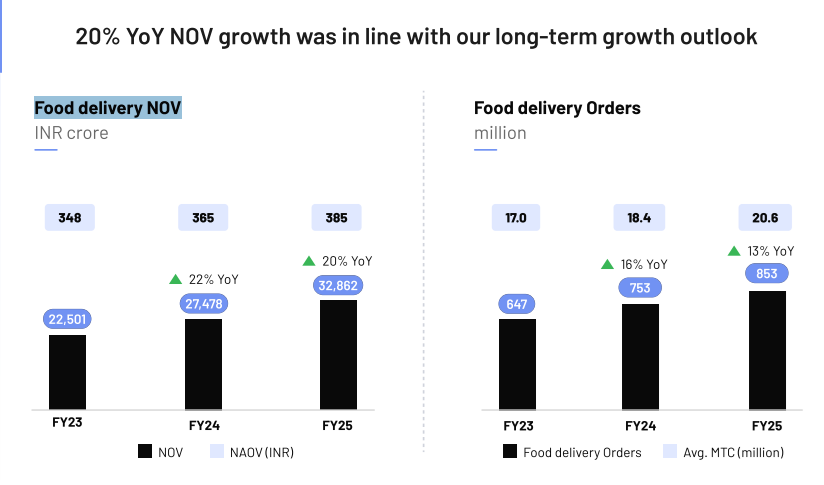

2. Food Delivery: The Engine That Finally Started Printing Money

1. Higher AOV → Higher Contribution Margin

AOV has stayed consistently healthy because:

India’s dining habits changed

Gold members order more frequently

Inflation was passed to consumers smoothly

Mix shift toward higher-value categories

Every +₹10 increase in AOV improves contribution margins dramatically.

2. Delivery Cost Fell Without Cutting Quality

This is Zomato’s secret weapon.

Delivery cost per order dropped because:

Higher order density → riders travel fewer kilometres

Route clustering

More predictable kitchen zones

Efficient batching

Better incentives design

Even a ₹2 improvement per order becomes massive at 1B+ annual orders.

3. “Gold” Finally Worked

Gold in 2019 was a disaster.

Gold in 2024–25 works because:

Zomato removed freebies

Encouraged frequency, not discounts

Gold fees became a recurring revenue stream

Gold reduces CAC dramatically.

4. Restaurants Now Pay More

Take Rate increased without merchants complaining because:

Restaurants depend on Zomato for 30–40% demand

“Growth ads” inside the Zomato app sell guaranteed visibility

Better dashboard tools sell at a premium

More merchant revenue → higher margin.

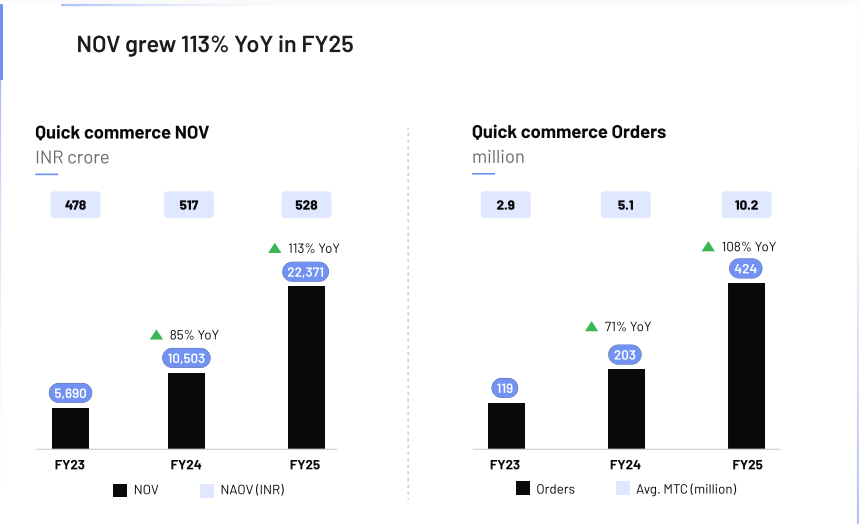

3. Blinkit: The Profitability Catalyst No One Expected

Blinkit is still reporting negative EBITDA today - but that’s not the real story.

The real story is that:

Contribution profit is already positive,

Losses have shrunk massively YoY,

Store density is improving unit economics

And Blinkit will likely turn EBITDA positive before food delivery did.

Blinkit NOV grew >100% YoY

And the magic?

Quick commerce has much better unit economics than food delivery. Why?

1. Higher AOV (₹550–650)

Quick commerce baskets are bigger than food.

2. Inventory margins

Blinkit earns money on:

product markups

ad placements

supply chain efficiencies

3. Store density = lower cost per order

More stores → closer to customers → cheaper delivery.

4. Instant delivery = higher frequency

People order impulsively:

milk

bread

snacks

stationery

home essentials

High frequency = recurring revenue.

Blinkit is on track to become EBITDA profitable before food delivery did.

This is the biggest sentiment shift for investors.

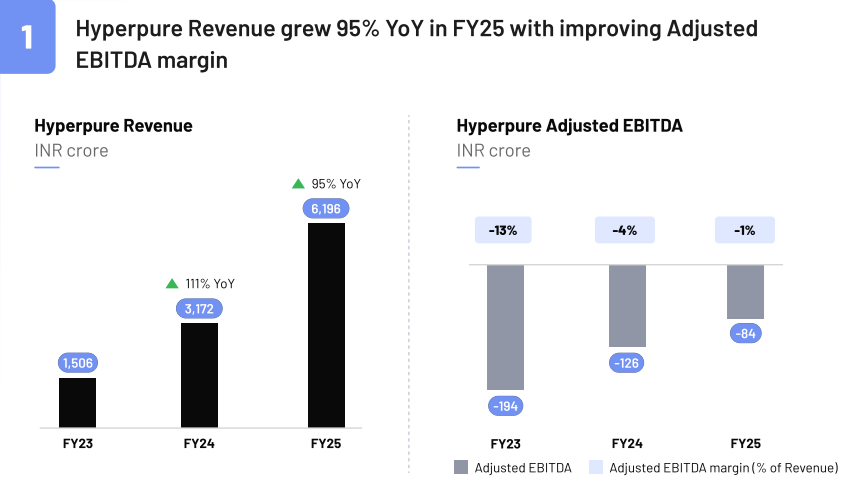

4. Hyperpure + Going-Out: The Silent Compounding Layers

Neither Hyperpure nor Going-Out is profitable yet - and that’s completely fine. What matters is the trajectory, not the snapshot.

Hyperpure revenue has doubled YoY

Going-Out is a high-margin, asset-light business

Both segments are scaling fast

They would not drive profitability today, but they would meaningfully strengthen Zomato’s margin profile over the next 2–3 years.

Hyperpure

Zomato supplies groceries & ingredients directly to restaurants.

It improves margins because:

one customer (a restaurant) buys in bulk

minimal marketing

predictable demand

lower delivery cost per kg

Hyperpure revenue doubled YoY.

Going-Out (District by Zomato)

Zomato earns from:

ticketing

event partnerships

dine-out bookings

nightlife passes

This is high-margin, asset-light revenue.

Zomato is slowly building an ecosystem beyond food delivery.

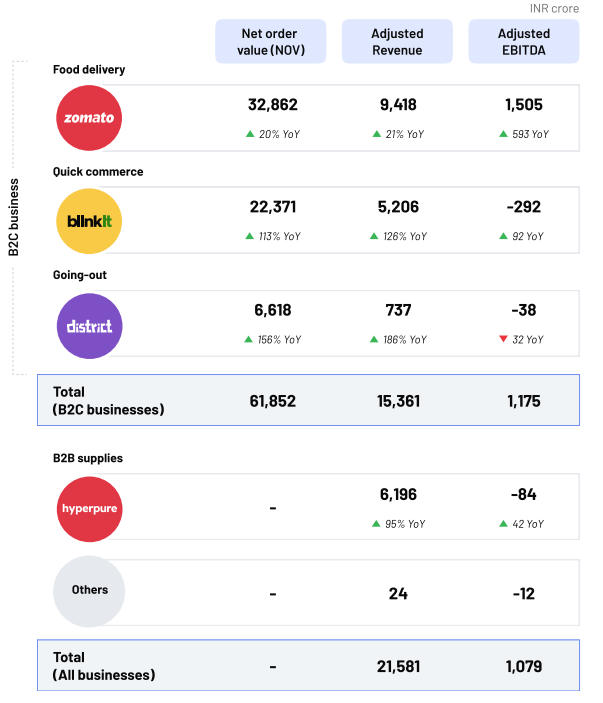

5. Business Model Summary - Where Zomato’s Money Actually Comes From

Zomato today is no longer just a food delivery company. Its revenue now comes from four different growth engines, and together they created the profitability flywheel that changed the company’s trajectory.

1. Food Delivery - The Stable Core

Still the largest revenue contributor.

High-frequency + strong AOV + optimised delivery costs = steady cash generator.

2. Blinkit - The Fastest-Growing Engine

Now contributes a rapidly rising share of total revenue.

Quick commerce is scaling much faster than food delivery.

3. Hyperpure - The Silent B2B Compounder

High-volume, low-volatility revenue from restaurant supply.

Improves profitability structure because of bulk order economics.

4. Going-Out (District) - Small but High-Margin

Event tickets, live experiences, dine-out bookings.

Asset-light + strong consumer engagement.

Zomato’s revenue is no longer dependent on ONE business line. The portfolio effect reduces risk and improves earnings quality, a key reason markets reward Zomato with a premium valuation.

6. Zomato vs Swiggy - The Reality Check

Food Delivery Market Share

Zomato: 55–57%

Swiggy: 43–45%

Quick Commerce Market Share

Blinkit: 35–36%

Zepto: 20–22%

Instamart: 32–34%

Zomato leads in the fastest-growing segment (quick commerce).

Profitability

Zomato = consistent profits

Swiggy = profitable but occasional fluctuations

Zomato wins on:

lower marketing spend

better cost control

higher density

more optimised Gold program

superior capital allocation

7. Simple Math: How One Order Turns Profitable

Let’s assume:

AOV = ₹420

Restaurant commission = 18%

Delivery fee (customer) = ₹35

Gold impact: -₹8

Delivery cost = ₹65

Discounts: -₹10

Payment + support cost: -₹7

Math:

Revenue per order = ₹420 × 18% + ₹35 = ₹110.6

Costs per order = ₹82

Contribution profit = ₹28.6 per order

Multiply this by 1 billion annual orders → ₹2,800 crores contribution before operating expenses.

THAT is how profitability suddenly appears.

8. Risks to Watch

1. Quick Commerce Bubble risk

If stores expand too fast → losses.

2. Competitive aggression

Zepto + Instamart may burn money again.

3. Regulatory pressures

Food delivery pricing scrutiny.

4. AOV stagnation

If AOV drops, contribution margins can collapse.

9. Valuation: Is Zomato Expensive?

Zomato trades at a high P/S (Price-to-Sales) multiple because:

A profitable Indian tech monopoly is rare

Quick commerce is booming

Hyperpure + Going-Out adds optionality

Strong cash reserves

Minimal competition long term

Peer context:

SaaS companies trade at 12–20× P/S

E-commerce companies often at 4–8×

Quick commerce globally is still unprofitable

Zomato (with profitability + growth) justifies a premium valuation

Is it expensive?

Yes, relative to earnings.

Is it justified?

Partially - due to dominant position & high-growth categories.

10. The Bottom Line

Zomato became profitable because it:

Increased AOV

Reduced delivery cost

Scaled Blinkit

Stabilized Gold

Raised merchant monetisation

Grew Hyperpure

Expanded Going-Out

Achieved massive order density

Stopped unnecessary marketing burn

Allocated capital brilliantly

This is a case study in how to turn a loss-making startup into a cash machine - using discipline, math, and strategic bets.

*Disclaimer: This analysis is for educational purposes only and is not investment advice.

IPO Investor’s Playbook is Here - Make Smarter IPO Decisions

I have launched my IPO Investor’s Playbook. It is a simple, practical guide with real case studies and a checklist that will help you understand IPOs better, avoid common mistakes, and make smarter, more confident investment decisions. You can check full details here: https://tinyurl.com/IPO2026Guide

Thanks for spending time with The Finance Lens! If this piece helped you, tap the ❤️, share it, or repost it on Substack; it really helps our insights reach more thoughtful readers like you. If you haven’t already, subscribe for free to stay up to date on our latest stories and insights. Because investing wisdom grows stronger when it is shared. 😊

Nice Analysis, hope you should have spent lot of time in it.

The only thing apart from all the positive side is that these company don't have a MOAT.

Currently local hotel associations are threatening Swiggy & Zomato in Tire 2 & Tire 3.

For example: As of July 2025, restaurants in Namakkal town and taluk(Tire 3 town in Tamilnadu) officially stopped supplying food to major delivery platforms like Swiggy and Zomato.

If Rapido (entering delivery business currently) decreases the fee for competition then Swiggy & Zomato has to, because customers are not loyal to these companies, they just need cheap.

Remember No founder of best performing business exit, but Deepinder Goyal have ejected through parachute from his captain seat is a high warning sign.

Swiggy, Zomato, Paytm - They don't have a MOAT or Competitive Advantage.

The cheaper survives - But cheaper services means making loss by burning cash.

If Food delivery is really a profit making business, Amazon, Flipkart & Bigbasket won't be watching it, they would have disrupted the industry by jumping in, but they are still in watch mode.

A 30 Billion USD valuation is still unjustifiable for this company! I don't know still how many years it takes for them to justify today's valuation.