How to Catch Multibagger Stocks Early: A Realistic Guide for the Patient Investor

“Multibagger don’t emerge from stock tips. They emerge from a quiet conviction, fundamental patience, and deep understanding.” — A value investor's notebook

If you have been investing for a few years, you have likely had this thought at some point: “I wish I had bought XYZ stock earlier.” Maybe it was Titan in the 2000s, or Deepak Nitrite in 2014, or even GMM Pfaudler before the chemical capex cycle began.

The idea of catching a multibagger early is the holy grail of equity investing. But let’s get honest — it is not easy, it is not fast, and it is definitely not luck. What it is, however, is achievable — with the right framework, a grounded mindset, and a keen eye for patterns that the crowd ignores.

First, What Makes a Multibagger?

A multibagger is simply a stock that multiplies your capital. A 2x is nice. A 10x can change your financial life. But multibaggers are not just fast growers. They are compounding machines that combine:

Consistent earnings growth

Increasing capital efficiency

Business tailwinds

Smart capital allocation

And most importantly — time

You do not need to swing for a 10x in a year. Even a stock compounding at 26% annually becomes a 10x in 10 years. The trick is catching them early, before the market has priced in their future.

A Realistic, 6-Part Framework to Spot Multibaggers Early

1. Start Small, Think Big: Market Cap and Business Scalability

“The bigger the runway, the bigger the potential.” — Peter Lynch

Most multibaggers begin small — often under ₹1,000 crore market cap — operating in boring or fragmented sectors. What separates them is a business model that can scale without linearly scaling costs.

Example: APL Apollo Tubes

In 2010, it was a basic steel pipe company.

It quietly built a pan-India distribution network, launched high-margin value-added products, and automated its plants.

Between FY12 and FY21, net profit grew 13x, and RoCE remained above 20%.

Market Cap rose from ₹200 crore to over ₹40,000 crore.

Early sign: Low base + large TAM + low cost of growth

2. Visionary Promoters with Skin in the Game

Multibaggers do not emerge from “professional management” alone. The early compounding phase is often led by founder-promoters with deep skin in the game and even deeper domain knowledge.

Look for:

Promoter holding >50%

Zero or minimal pledging

No reckless dilution or equity raises

Promoters buying from the open market

Example: Vijay Shekhar Sharma in Paytm vs. Promoters at Page Industries

While Paytm had vision, it was overly dilutive and lacked profitability for years. Compare that to Page Industries, where promoters scaled the Jockey franchise in India without debt, without hype, and with rising profit per rupee of sales.

3. Margin Expansion and Operating Leverage: The Invisible Booster

Here is a hard truth: revenue growth is overrated. The real multibagger kicker is margin expansion, when profits grow faster than sales, due to operating leverage or pricing power.

Example: Deepak Nitrite (2014–2020)

Revenue CAGR: 14%

Net Profit CAGR: 60%

How? Shift from commodity products to niche chemicals, better asset utilisation, and disciplined cost control.

Early sign: EBITDA margin inching up YoY without pricing gimmicks

4. Rising RoCE with Low Debt: The Sign of a True Moat

No business can compound sustainably without capital efficiency. One of the earliest signs of a multibagger in the making is rising Return on Capital Employed (RoCE) and declining debt.

A company with RoCE >18% and reinvestment opportunities has a mathematical edge in compounding.

Example: Dixon Technologies

RoCE stayed above 20% as they scaled contract manufacturing

Capital-light business model (no inventory risk)

Huge optionality with government PLI schemes

5. Under-Ownership: The Calm Before the Storm

If you want outsized returns, you must buy before the institutions do. Early multibaggers usually have:

<5% institutional holding

Zero or minimal analyst coverage

No media buzz

Quietly compounding earnings

Example: GMM Pfaudler (pre-2018)

Operated in industrial glass-lined equipment (niche B2B space)

Became a proxy to India’s speciality chemical capex boom

Institutions began chasing the stock post-2019

Early sign: Stock with rising EPS and flat P/E (valuation gap)

6. Catalysts: Tailwinds, Turnarounds, and Timing

Even a great company needs a push. This comes in the form of industry tailwinds, government policy shifts, or strategic pivots.

Example: Syrma SGS Technology

Operated in niche EMS (electronics manufacturing services)

PLI Scheme + global China+1 shift = perfect macro tailwind

Huge optionality with design + manufacturing + exports

Early believers got in before it hit mutual fund radars

Early sign: Strong promoter-led pivot + policy tailwinds

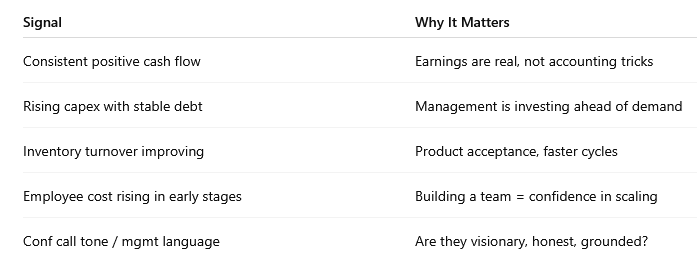

Beyond the Screener: Real Clues in the Footnotes

You can not find multibaggers by filtering “P/E < 10” or “Sales CAGR > 20%”. You need to read the footnotes, not just the ratios.

Look for these subtle signals:

What Multibaggers Don’t Look Like

Here is where most investors fall into traps:

Chasing low P/E commodity stocks that are profit-cyclic

Falling for turnaround stories without management change

Assuming every small-cap is underpriced

Buying hyped-up names without reading the annual report

Remember: Every stock that is down 80% was once someone’s multibagger dream.

Final Thoughts: Patience Is the Alpha

Catching a multibagger early is like planting a sapling, not buying fireworks.

You must be willing to:

Buy when the stock is boring

Hold through flat or choppy phases

Track execution, not just price

Avoid overtrading and anchoring

If you find one true multibagger every 5 years, you will outperform most.

So, stop chasing the next quick 2x. Start observing, reading, questioning, and holding — that is how early wealth is built.

This article shares my personal views and analysis, not investment advice. Always do your own research or consult a financial advisor.

I write regularly on investing fundamentals, market behaviour, and real-world insights. Follow me on X @SmitaP07 and subscribe at theequityecho.substack.com for clear, honest analysis.