Insurance Sector Decoded: The Hidden Gem Most Investors Ignore

A simple, real-world guide to understanding how the insurance sector works, what drives its growth, and how investors can spot real opportunities.

Hello and welcome back to The Finance Lens!

Ever wondered why insurance companies — the ones we rarely talk about — quietly hold some of the most powerful balance sheets in the country? While we chase the next big IPO or tech stock, this sector continues to compound steadily behind the scenes.

In this post, I will guide you through how to analyse the insurance sector like a pro — from understanding what drives its growth to decoding key ratios, identifying challenges, and determining which companies truly deserve your long-term attention.

Let’s break it down — the calm, steady world of insurance that keeps the financial system from falling apart.

What We Will Cover Today

Here’s a quick look at what’s inside this article:

What the Insurance Sector Really Is — and why it quietly powers India’s financial backbone.

Key Growth Drivers — from rising income levels to digital transformation and government reforms.

Major Challenges — the real-world hurdles insurers face, from low awareness to tight regulations.

Essential Ratios & Metrics — how to read solvency, persistency, and claim settlement like an analyst.

Top Players in the Industry — LIC, HDFC Life, ICICI Lombard, and more.

Future Outlook — the trends shaping insurance in the next decade.

Management Quality & Investor View — what to look for before investing in an insurance stock.

By the end, you will understand how to look at this sector not just as a policyholder, but as an informed investor.

Don’t just read once—stay connected. Subscribe for free to get thoughtful insights, fresh ideas, and more stories like this in your inbox.

Introduction

Insurance is not the most exciting topic to talk about, let’s be honest. When people think of finance, they picture stocks, crypto, or fancy startups — not insurance policies and claim ratios. But if you have ever been in a hospital bill shock or seen a business lose everything after a fire, you understand why this sector quietly holds the economy together.

The Indian insurance industry is actually a sleeping giant. With over 1.4 billion people and growing income levels, the opportunity here is massive. Yet, insurance penetration is still low — roughly 4% in life and about 1% in non-life. That’s like having a full buffet, but most people are still eating just rice. The gap is the opportunity — and that’s what makes this sector worth studying.

Key Drivers

Now, what makes insurance tick? A few things:

Rising Incomes & Awareness – As people start earning more, they begin thinking about health, life, and what happens “if something goes wrong.” I still remember when my cousin got her first salary — she bought a health policy before buying her first gold ring. That shift in mindset is exactly what drives this sector.

Government Push – Schemes like Ayushman Bharat and PM Bima Yojana are pushing insurance into rural corners. You would be surprised how many families in small towns now have basic coverage.

Digital Everything – Buying policies are no longer about filling out 10 forms in a dusty office. You can compare, buy, and renew insurance online in minutes.

Urbanisation & Credit Growth – More homes, more vehicles, more loans — and naturally, more need for insurance.

Tax Perks – Let’s admit it, most people start their insurance journey not for safety, but to save tax. Whatever the reason, it helps the sector grow.

Challenges

Of course, it is not all smooth sailing. Insurance companies face a few stubborn problems:

Low Awareness – Many still see insurance as an “extra expense,” not protection.

Complex Jargon – Ever tried reading a policy document? It feels like decoding a secret language.

Fierce Competition – Price wars and mis-selling eat into profits.

Regulatory Tension – IRDAI keeps a tight leash on pricing, commissions, and product design. It is necessary, but it often limits flexibility.

Market Volatility – Since insurers invest heavily in markets, a crash can hit their balance sheets.

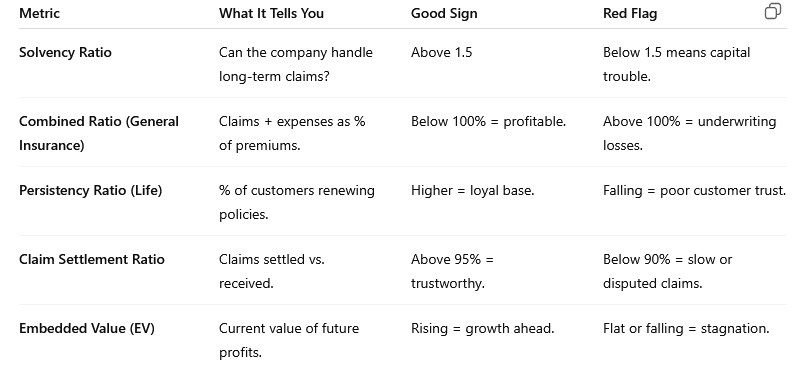

Key Ratios / Metrics

Now, if you are analysing an insurance company, numbers tell the story. But not all ratios are equal — here are the ones that matter:

One small personal tip: I always start by checking the claim settlement ratio first. Numbers don’t mean much if the company doesn’t actually pay when people need it.

Major Players

The space is dominated by a few big names:

Life Insurance: LIC, HDFC Life, SBI Life

General Insurance: ICICI Lombard, New India Assurance, Bajaj Allianz

Health Specialists: Star Health, Care Health

LIC still commands massive trust (my parents would not even consider anyone else), while private players are chasing growth through digital innovation and personalised plans.

Future Outlook

The next decade looks exciting.

IRDAI’s Vision 2047 aims for “Insurance for All,” which sounds ambitious, but with India’s speed of digitisation, it might just happen.

Tech is transforming everything — AI-driven underwriting, telematics in motor insurance, even wearable data in health plans.

Post-COVID shift – People now value health cover more than ever.

Global Trends: Climate change is also forcing insurers to rethink coverage models — for crops, floods, and natural disasters.

Most analysts expect the Indian insurance industry to grow at a 10–12% CAGR in the next 10 years. That’s faster than many traditional sectors.

Management Matters

When you study insurance companies, the management deserves extra attention.

Good leaders focus on customer trust as much as profit. Check if they have maintained steady premium growth and claim settlement over the years — not just one lucky year.

Also, look at promoter ownership and transparency. If management keeps communication clear and doesn’t play hide-and-seek with numbers, that’s a huge plus. Incentives should reward long-term growth, not just flashy sales.

Investor View

So, should you invest in this sector?

If you are someone who believes in steady compounding rather than quick profits, insurance stocks might fit you well. They reward patience. Think of it like owning a business that earns quietly in the background — one premium at a time.

Risks: regulatory curveballs and market-linked investment losses.

Rewards: strong balance sheets, recurring income, and deep structural growth.

If you can hold your patience for 5–10 years, this sector can be surprisingly generous.

Final Thoughts

Insurance may not be glamorous, but it is the calm behind every financial storm. It is what lets economies recover, families rebuild, and businesses restart.

The irony is — people only appreciate it after something goes wrong. But investors who understand this sector early often find their returns compounding quietly while others chase the next big trend.

So maybe, the next time someone calls insurance “boring,” smile — because you know boring often makes the best money.

Thanks for spending time with The Finance Lens! If this helped, subscribe for free to stay up-to-date with our insights. And if someone in your circle could also benefit from this, share it with them—because investing wisdom grows stronger when it is shared.

The low penetration numbers you mentioned really hit home when you think about the scale of the oportunity. Bajaj Allianz and the other general insurers are positioned well to capture that growth as urbanisation accelerates and more people need coverage for assets and vehicles. What resonates with me is the shift from insurance as tax saving to insurance as protection mindset you described becuse that behavioral change unlocks real pricing power. The claim settlement ratio focus is spot on, trust drives everything in this sector and no amount of digital innovation can replace that fundamental.